Hey guys!

Like the title says, I would love some help on this quite general problem for me. Too often while building models (mostly Keras), I end up in a situation where I manage to get both training- and val loss down to about 0.5 (this time for a rather simple regression problem), but then it starts to oscillates and I am unsure of how to proceed.

I am using this Kaggle dataset: Housing Price Prediction Data | Kaggle

What I’ve tried to far:

Many different network architecture (started out simple and made it gradually deeper/wider), but of course, I might have missed a sweet spot.

Added Dropout, L2-reg and switched from Relu to Leaky Relu

Fiddled around with the learning rate quite a bit - now using both a ReduceLROnPlateau and a scheduler.

Tried different batch sizes (between 32 and 256).

Tried SGD instead of Adam, then switched back.

Tried changing the number of epochs (ranging from 50 to 200).

Code:

Early stopping

early_stopping_callback = EarlyStopping(monitor=‘val_loss’, patience=35, verbose=1, restore_best_weights=True)

Reduce learning rate on loss plateau

reduce_lr = ReduceLROnPlateau(monitor=‘val_loss’, factor=0.1, patience=15, min_lr=0.0001, verbose=1)

opt = Adam(learning_rate=0.0001)

Add the learning rate scheduler to the callbacks

scheduler_callback = LearningRateScheduler(lambda epoch: 0.001 * np.exp(-epoch / 10.))

Batch size

batch_size = 128

Regularization factor

l2_reg = 0.001

%% Set up model

model = Sequential([

Dense(16, kernel_regularizer=l2(l2_reg), input_shape=(X_train_scaled.shape[1],)),

BatchNormalization(),

LeakyReLU(alpha=0.01),

Dropout(0.1),

Dense(48, kernel_regularizer=l2(l2_reg)),

BatchNormalization(),

LeakyReLU(alpha=0.01),

Dropout(0.15),

Dense(80, kernel_regularizer=l2(l2_reg)),

BatchNormalization(),

LeakyReLU(alpha=0.01),

Dropout(0.2),

Dense(80, kernel_regularizer=l2(l2_reg)),

BatchNormalization(),

LeakyReLU(alpha=0.01),

Dropout(0.2),

Dense(80, kernel_regularizer=l2(l2_reg)),

BatchNormalization(),

LeakyReLU(alpha=0.01),

Dropout(0.15),

Dense(64, kernel_regularizer=l2(l2_reg)),

BatchNormalization(),

LeakyReLU(alpha=0.01),

Dropout(0.15),

Dense(1, activation='linear', kernel_regularizer=l2(l2_reg))

])

model.compile(optimizer=opt, loss=‘mean_squared_error’, metrics=[‘mean_absolute_error’])

%% Train model

history = model.fit(

X_train_scaled, y_train_scaled,

epochs=80,

batch_size=batch_size,

validation_data=(X_val_scaled, y_val_scaled),

shuffle=True,

callbacks=[checkpoint_callback, early_stopping_callback, scheduler_callback, reduce_lr]

)

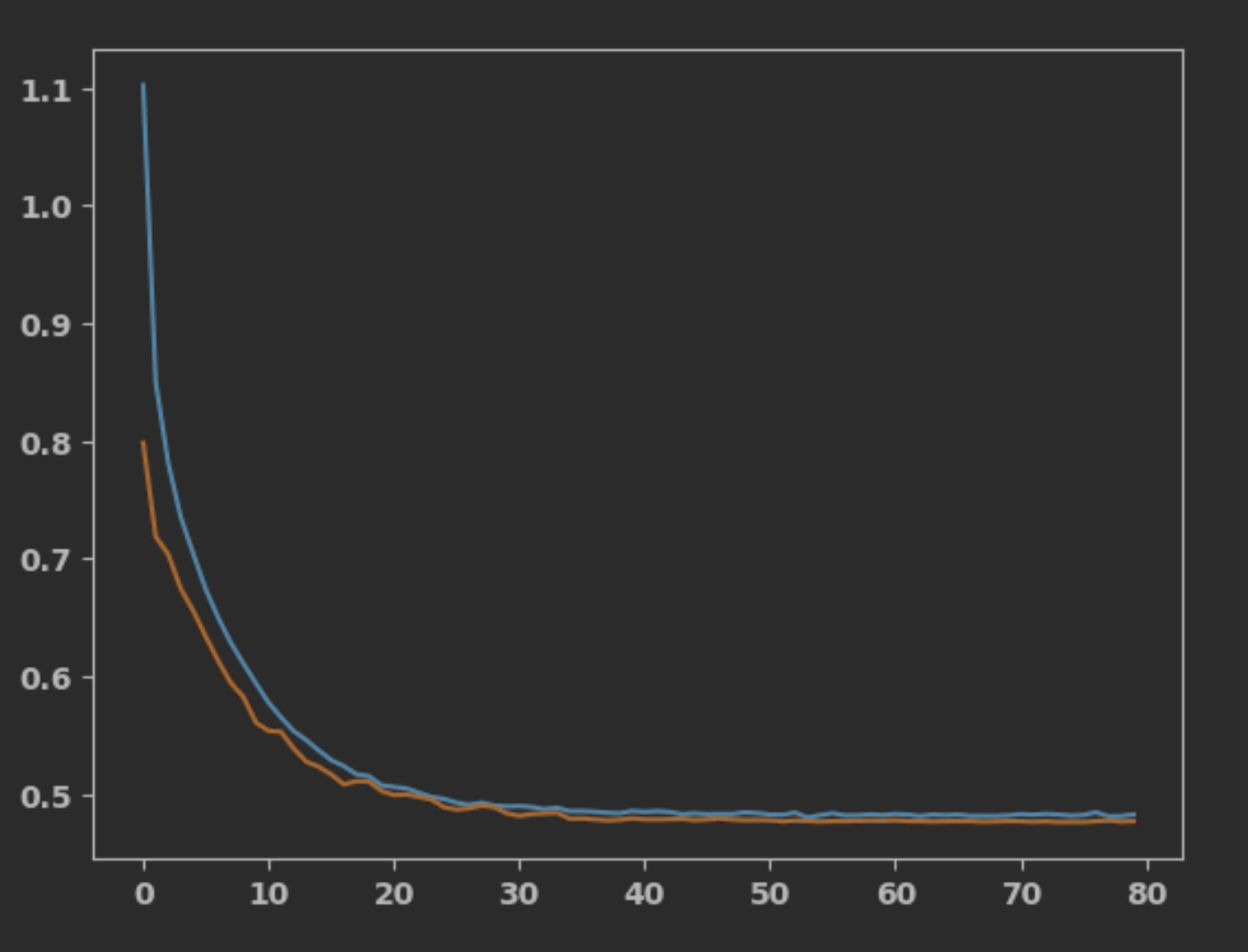

Loss:

I would highly appreciate any tips or help to get around this problem. From what I understand it’s quite common. Many thanks in advance!